BYU Student Health Insurance loses ACA status: What every student needs to know

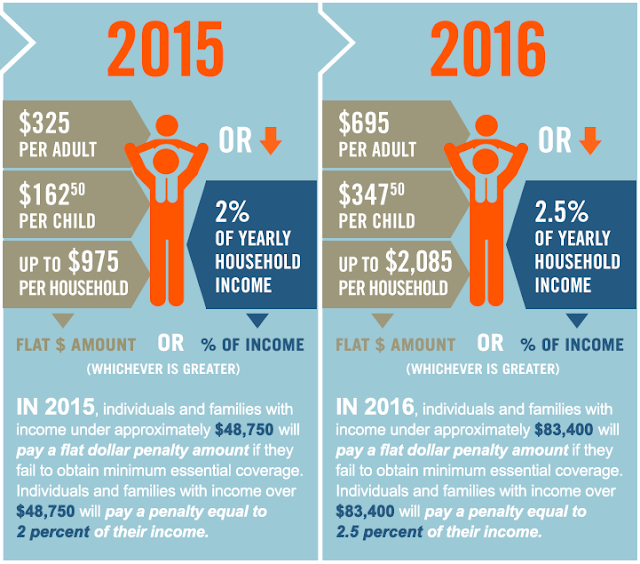

Newsflash--starting August 31, 2015, BYU Student Health Insurance will no longer qualify as "minimum essential coverage" under Obamacare or the Affordable Care Act. BYU hasn't really done much to advertise this fact or its potential tax ramifications on students. I have wasted a couple hours of my life trying to figure out what this means for me. Hopefully, I can save you some time. Wait, is this for reals ? Yep. From BYU's own website: To meet the ACA medical coverage requirement, a health plan must qualify as “minimum essential coverage,” which is a type of health coverage approved by the federal government. Beginning August 31, 2015, the BYU Student Health Plan will no longer be considered minimum essential coverage. [I find this next part funny...] Although the BYU Student Health Plan will not meet the ACA requirements, it will continue to meet the university’s health coverage requirement. [Good to know BYU isn't about to sell you insurance that ...